Have no fear! It’s not all doom and gloom on the real estate market front.

It looks like the Fed has relaxed on interest rate hikes and things are finally starting to level out in the market. I’m not calling myself Nostradamus or anything, but in my March blog post on the state of the Portland real estate market, I predicted there would be a short window of opportunity to sell your Portland home right before interest rates were anticipated to go up. That time has since passed, and homeowners are currently finding it more difficult to sell.

If you’re new here, I’m Lauren Goché — a Portland realtor with a decade of experience backing me up. Which means I’ve weathered more than a few market shifts over the course of my career, and specialize in making sure you can make the most of the market for your goals. Read more about me here.

It’s a Great Time to Be A Buyer — Here’s Why.

I have to be honest, I wasn’t sure if buying now was something I was willing to recommend, which is part of why I hesitated to post this earlier… But I can now confidently say I’ve made a complete 180° — it’s a GREAT time to be a buyer. Yes, interest rates are higher than you’re used to seeing in the last two years, but here is something you haven’t seen. Right now, buyers have a rare upper hand to negotiate that we haven’t really seen in the past decade.

After seeing my buyers score great deals in this market, I realized that there’s more to these market conditions than meets the eye. So I called up my lending friend and confidant, Jen Leon, to join me on a recent Instagram live (check it out here) and discuss what exactly Oregon realtors and lenders are saying about this market—and if I wasn’t convinced before, I am now. Jen is a mortgage advisor with a whopping 27+ years of experience and as a Portland native, they have an amazing grasp on what’s happening in the local market. You can check them out over here at Guild Mortgage. NMLS #41237

Keep on reading if you want our 4 main reasons you should BUY NOW!

1. You Have the Power to Negotiate

Right now, my buyers are not only closing on the home they couldn’t compete for in last year’s market, they’re getting it with big buydowns, big repairs, and reduced closing costs. These are called seller concessions because the seller covers the cost in order to incentivize you as a buyer. This is resulting in HUGE savings for my buyers, the likes of which I haven’t seen for YEARS.

Here are some of the programs and tools my buyers have been using:

Lower your mortgage with a 2-1 buydown

You can get your seller to pay for a 2-1 buydown which allows you to make a lower mortgage payment for the first 2 years of their loan. Say your overall interest rate is 7%—with a 2-1 buydown, for the first year in your home, you only have to pay 5%. The next year you pay at 6% and then after that, it stays at 7% for the rest of eternity. This is especially beneficial for those buyers who know their income is going to increase reliably in the next few years.

Get your seller to pay for closing costs

Did you know you can negotiate with your seller to pay for some, or all, of the closing costs? This was rare in the last decade since sellers had plenty of interested buyers to choose from. So take note that once there are multiple offers again, this goes out the window! Here are fees included in closing costs that you can negotiate with the seller:

- Origination fees

- Discount points

- Homeowner’s insurance

- Loan application fees

- Title insurance

This is where having a realtor comes in handy. Your realtor should be able to discuss all of these options with you and negotiate the best deal possible on your behalf.

Get necessary repairs paid for

Many sellers will pay for necessary repairs that come up during home inspections as a way to get you to seal the deal. Here’s a list of common repairs needed after home inspection. We think these should definitely be on your list to negotiate!

- Structural damage

- Water damage and mold

- Roof damage

- Broken appliances

- Plumbing, sewage, and septic problems

2. Buy Now, Refinance Later

The only sure thing about interest rates is that they fluctuate, so don’t let a high rate discourage you from buying your dream home! The rule of thumb is once rates are 1% lower or more than the rate you locked in, it’s time to refinance. Here are our insider tips to know about refinancing in this market!

Refinance for free!

Yes, you heard me! Jen reveals that lenders know that once interest rates go down, homeowners will rush to refinance. So to make sure you stick with the same lender in the case of a refinance boom, many of them are offering to reduce or get rid of their lender fees. This will literally save you thousands! You can contact Jen directly at Guild Mortgage about waiving your lender fees up until 2025 to refinance.

Remember the 2-1 buydown? You can still refinance!

As mentioned previously, you can get your seller to pay for a 2-1 buydown to reduce your mortgage costs for the first two years. You’ll receive the difference as a lump sum in the form of seller credit. This will let you buy some time until you’re able to refinance AND if rates go down before the two years are over, you won’t get penalized for refinancing early. You can take any seller credit left over and put it into your principal. Now that’s a sweet deal!

Our Strategy

If you ask Jen and me, our strategy is: buy the house, get a 2-1 buydown, and then refinance later. worst case scenario you’re locked into a 7% interest rate and it goes up to 10%, and you’re still in a better position than everyone else. Best case scenario rates drop to 5%, and you refinance and lock it in at 5%.

3. Be on the Lookout: Competition Will Increase!

As interest rates are starting to slowly decline, Jen and I have encountered two types of buyers:

Buyer 1 – thinks interest rates are going to fall further, so they decide to wait…

Buyer 2 – is super savvy and says, “Yeah, the interest rates are up, but that means more time for me and more pressure on the seller to lower prices. I can get all the things I couldn’t get 8-10 months ago!”

Our theory is: this market gives you time to make good moves, negotiate, and work with your agent without feeling pressed. For those who want to play the waiting game with interest rates, keep in mind, if rates come down to the 5% range, we are going to see buyer pools starting to grow.

Here’s why we don’t recommend waiting:

Housing inventory is still low

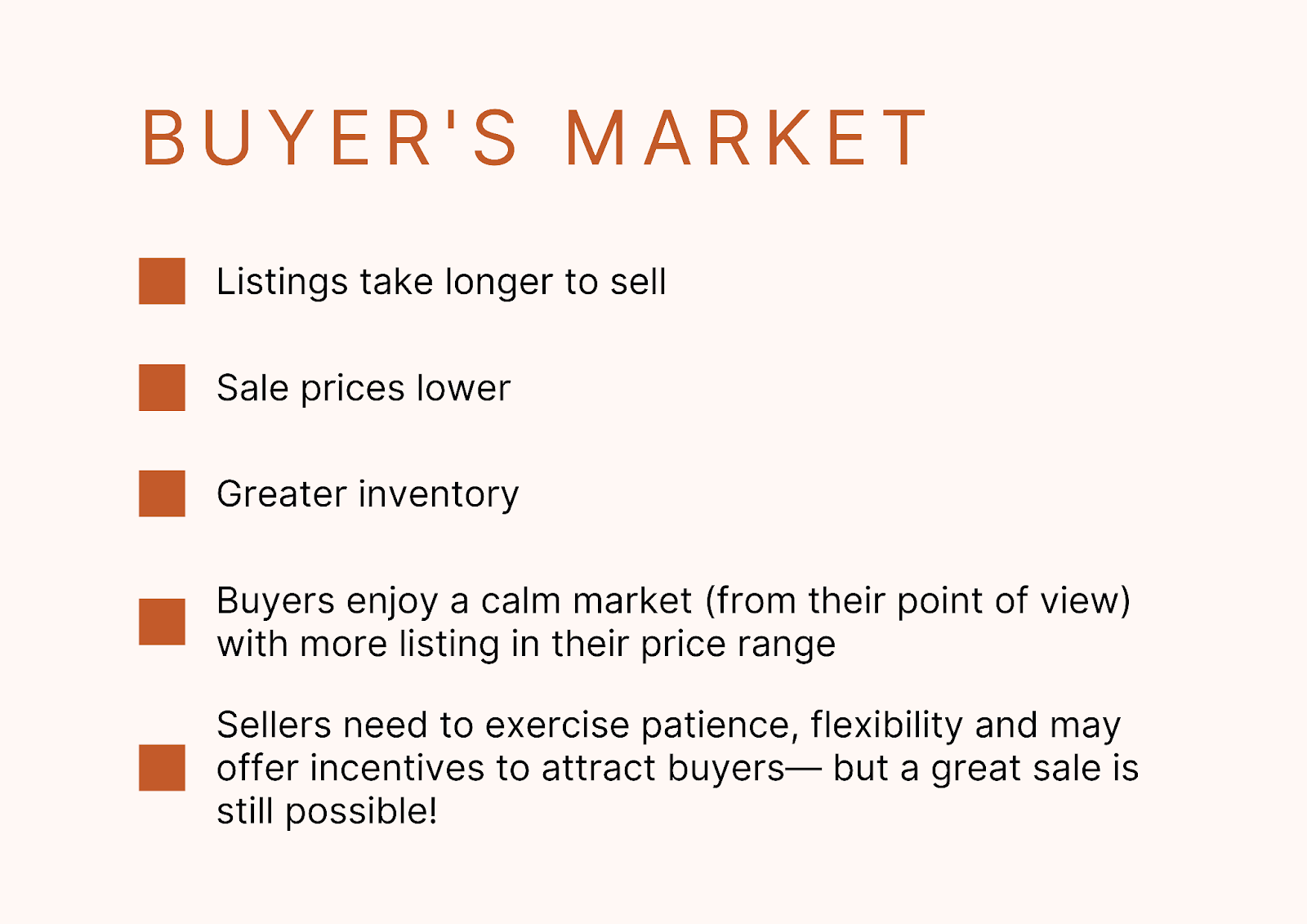

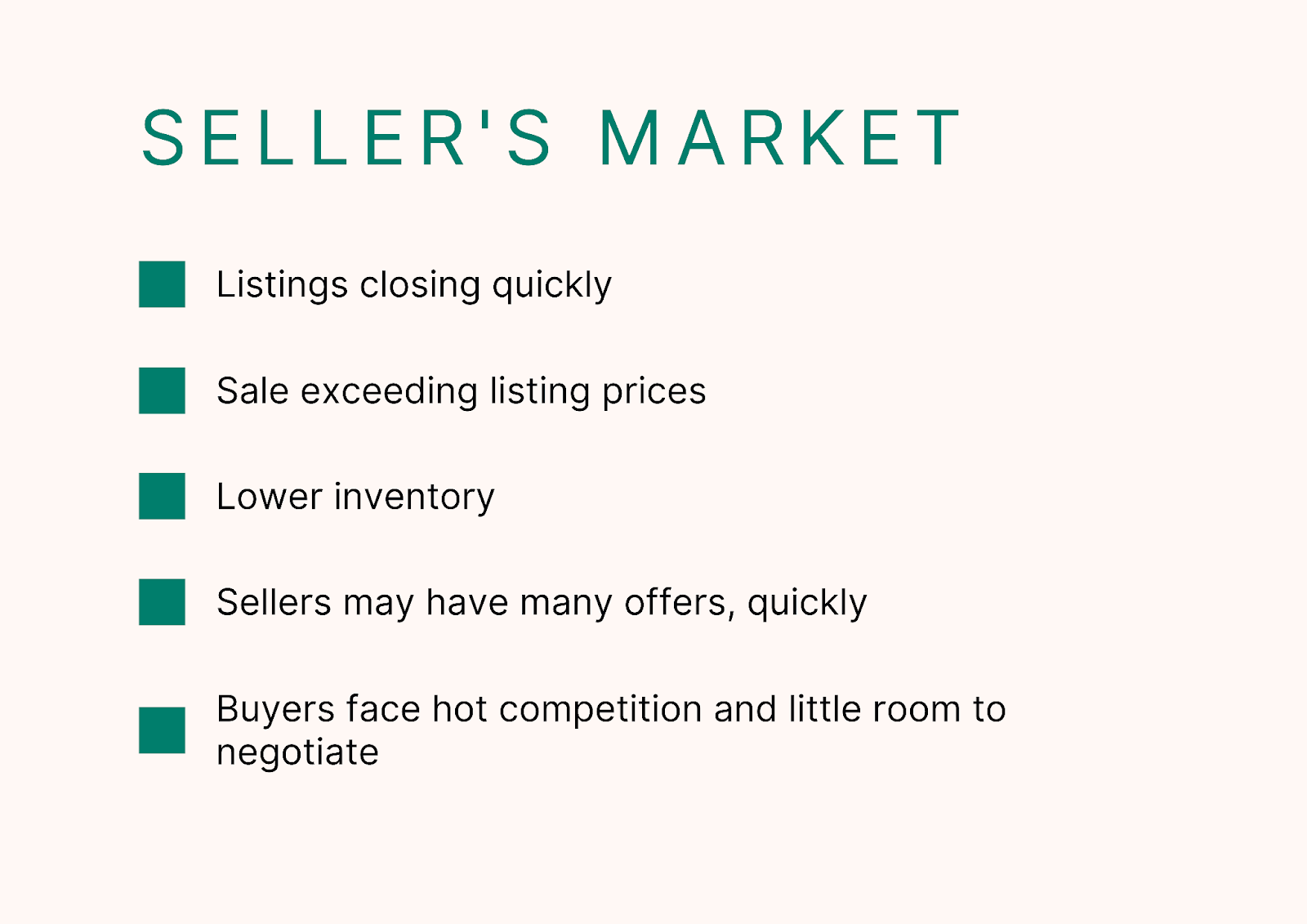

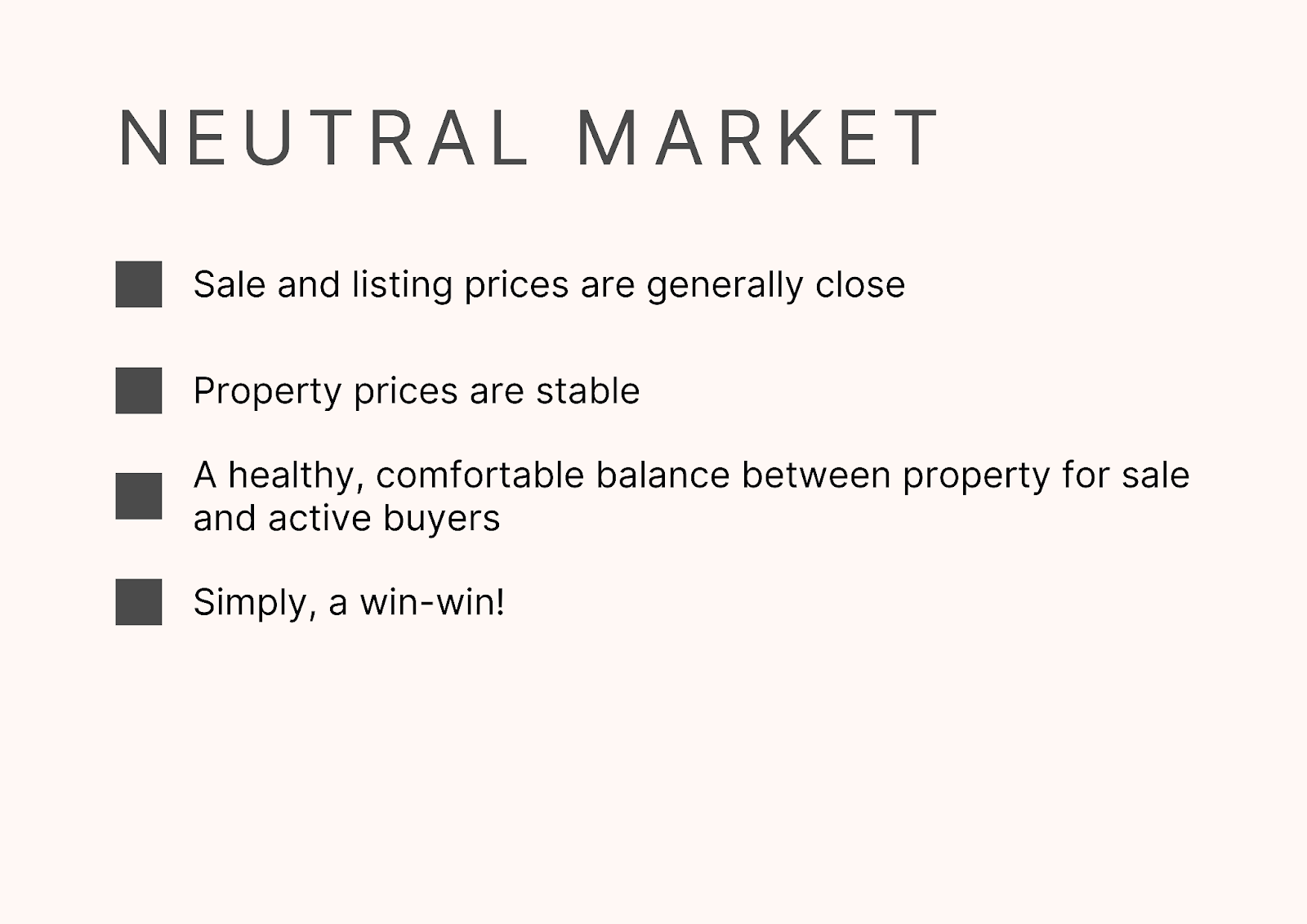

Even though we are telling you it’s a great time to buy, there are still not enough properties on the market to technically make it a buyer’s market. We’re currently at a 2.5 month inventory and rising. I consider 4 months of inventory and under as a seller’s market; 6 months and over as a buyer’s market; and 4-6 as neutral. So why does it feel like a neutral market? Well, that’s because high interest rates are keeping demand low.

If you need a refresher, here’s a simple breakdown and key indicators of buyer’s markets, seller’s markets, and neutral markets:

Interest rates could decrease

When interest rates get back down to 5%, more people can qualify to get back into the game. Couple that with low inventory and we’re looking at entering a seller’s market again. That means added competition, more stress, and less time for you as a buyer. Although it may seem counterintuitive, high interest rates are what’s leveling out the playing field for buyers. So take advantage of it while you can!

4. Why You’re in a Better Position Than Buyers 2 Years Ago

Our takeaway for buyers is not to let these high interest rates scare you — if you buy now, you’ll be in a great position to sell later. Here’s why you’re in a better position than people who bought their home in the last two years:

Better price on your home

It’s true, you could get a good interest rate 10 months ago, but you probably overpaid on the house and weren’t in a position to ask for any repairs. If you buy a house now at a higher rate, but it’s only 5% above asking price, you will have an easier time selling in the future compared to someone who paid 20% above asking but got a low rate. Don’t forget that your future buyer might not be able to lock in the same low rate as you!

I always tell my clients that real estate is a long-term investment, keeping your home for 7-10 years will give the biggest bang for your buck. Yes — there have been times in the past few years when clients have sold their house within 2 years, but you shouldn’t build that into your real estate plan right now. It’s just not sustainable!

What’s the future like for the Portland Market? Well, I don’t have a crystal ball, but I’m sensing this spring will be more of a “typical” Portland spring market — rates will lower, buyers will come in, and inventory will increase. It will be more competitive, but nowhere near the last couple of years.

Our key takeaways:

- Buyers have the power to negotiate for seller concessions like getting a 2-1 buydown, having your seller pay for closing costs, and getting necessary repairs fixed.

- We recommend buying now, getting a 2-1 buydown, and then refinancing. You can refinance for free up until 2025 with Jen, and if you get a 2-1 buydown and refinance early, you can add the remaining balance to your principal.

- With housing inventory still low, it seems like high interest rates are keeping demand at bay and ultimately preventing us from entering a seller’s market. Once rates go down, competition will go up for buyers. So don’t wait!

- If you buy now, you’re setting yourself up for success when it’s time to sell! Buyers in the past two years got a low rate but likely overpaid for their homes.

You need an experienced lender and realtor to rely on while traversing the market. Can you tell I love working with buyers? I’m ready to help you find your next unique home in Portland — get in touch with me here!